African countries can leverage their natural gas resources to create a viable long-term investment pathway, particularly by capitalising on short to medium-term funding opportunities.

Among the diverse energy options for Africa, the abundance of natural gas and the proven efficiency of combined cycle gas turbines (CCGTs) in power generation make it a suitable complement to renewables in Africa's just transition plan, write Abubakar Abbas, Senior Energy Forecast Analyst, Gas Exporting Countries Forum (GECF) and Alexander Ermakov, Energy Econometrician, GECF.

However, realising the potential of natural gas requires significant upstream investment and long-term contracts, which some international investors were hesitant to undertake until recently, that IEA’s position emphasised the importance of expanding natural gas use for Africa’s industrialisation.

Increased production

It is important to note that the rising demand for natural gas in Africa will require increased production to meet domestic needs, with exportation to distant destinations as a potential option.

In spite of the underinvestment in the sector, African natural gas reserves are gaining significant attention for investment, with Africa targeted to supply European Union’s gas demand of up to 30 bcm by 2030 due to reduced dependency on Russian supply.

The recent surge in demand for African gas supply for the short to medium term due to geopolitical tensions is unclear. However, Africa must focus on the certainty that gas will be needed for the future, regardless of potential future events.

Africa's path towards a low-carbon future is clear yet limited. With a large population and the need for sustainable economic growth in the next three decades, Africa must address extreme poverty, which is at alarming levels globally and reduce emissions.

Least emissions

Africa contributes the least to global emissions. To meet these challenges, Africa requires an energy source that is abundant enough to meet the growing population's needs, reliable enough to provide continuous energy throughout the year, and affordable to address the dire needs of Africans. The combination of natural gas and renewables appears to be the key to meeting Africa's future energy demand.

Again, the link between African gas usage and the current climate change drive is completely not related. This is based on IEA’s insights during the African Energy Outlook launch in 2022: “If we make a list of the top 500 things we need to do to be in line with our climate targets, what Africa does with its natural gas does not make that list”. This has been said for all Africa’s future, heavily relying on natural gas without significant climate concern while generating adequate economic revenue to fund its just energy transition. Globally, the changing narrative in favour of natural gas investments is continuing across all regions.”

This can also be seen with the new EU parliament’s recent vote in favour of natural gas acceptability as a “green” tag. Gradual investment opportunities are sailing through, with the current 17 projects identified for investment partnerships in Africa, including Italy’s Eni’s agreement in Algeria, Egypt, and Congo, while Norway’s Golar signed MoU with Nigeria’s NNPC for floating LNG in April 2023.

More investments

Despite timely and encouraging decisions, more such investments are needed to meet the future energy needs of both on the global scale and in Africa.

Given the young, burgeoning, and rapidly urbanising African population and strong projected economic growth, the energy sector has a vital role to play in Africa’s future. According to the GECF GGO, the continent’s primary energy demand is expected to increase by 82% from 860 Mtoe in 2021 to 1,565 Mtoe by 2050.

Sub-Saharan Africa is expected to account for 84% of this growth amid higher living standards, signaling better access to energy and improvements in the energy poverty problems. Natural gas will be responsible for around 30% of Africa’s total energy demand increase – the most significant gain of any fuel. Natural gas endowment confirmed by a series of significant discoveries fits well with Africa’s push for industrial and social development. Africa will enjoy an LNG export expansion while resulting revenues will help to drive economic growth and structural transformation.

Pipeline construction

Enhancement and expansion of infrastructure could be a potential stumbling block, but a number of countries, both established gas producers and emerging ones with significant resource potential (to name a few, Mozambique, Tanzania, Senegal and Mauritania), have plans for pipeline construction and network development to stimulate domestic gas demand, despite the strong export orientation of the projects.

Simultaneously, in addition to long-distance pipeline development (e.g. the Trans-Saharan Gas Pipeline and the Mozambique to South Africa Pipeline), options such as gas-by-wire within the same regional power pool or small-scale LNG solutions will create new sources of demand allowing African nations to monetise locally produced gas and intensify intra-region integration.

With targets to ensure universal access to electricity and the need to meet the substantial power deficit, especially in sub-Saharan countries, power generation will provide the lion’s share of gas demand increase in the region.

Scope for gas

From an economic and environmental view, there is significant scope for gas to displace oil-fired generation, to constrain the expansion of coal-fired capacity in South Africa and its neighbours (where coal is a dominant source), and to enable accelerated electrification. Natural gas will also play an increasingly important role in sub-Saharan countries that continue to depend on hydropower, ensuring a backup during dry spells.

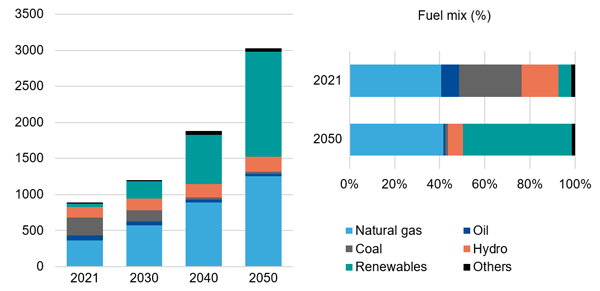

According to GECF estimations, electricity generation in Africa will surge from 890 TWh in 2021 to 3,025 TWh in 2050. Natural gas is forecast to cover more than 40% of the total growth and account for 42% of the regional power generation mix by 2050. In this regard, natural gas, in tandem with renewables (which will grow rapidly, underpinned by countries’ plans and supporting programmes and initiatives), will become essential in improving electricity access.

Rising gas availability will also encourage demand in gas-based industries such as petrochemicals, methanol, and fertilisers. Many industrial projects proposed for several sub-Saharan countries provide strong commercial cases for domestic gas market development. Simultaneously, natural gas as a key fertiliser input will contribute to agricultural sector productivity and play a role in ensuring food security. In addition, there is potential for gas to penetrate the residential segment while helping to move away from the use of traditional biomass, thereby alleviating air pollution and preventing deforestation.

Greatest opportunity

Overall, natural gas is assumed to be Africa’s greatest opportunity as a long-term energy solution to help alleviate energy poverty, enhance the quality of life and meet the expected economic growth. Investments and capacity building are the main prominent steps to take moving forward.

At the same time, while investments by both international and regional funders are eminent, there has been a skill gap in Africa that will continue to enable domestic technology and skills transfer among Africans. Africa has relied on other continents to meet its skilled labour in the energy sphere and moving forward will require a comprehensive policy approach to meet the critical needs of Africa for the future. This is in addition to waving a new prospect of Circular Carbon Economy (CCE) initiatives, particularly Carbon Capture Utilisation and Storage (CCUS) in designing the African pathway for a low-carbon future. In this context, adoption of natural gas, proven technologies, such as CCUS, and renewables will ensure accelerated economic growth, climate targets and the attainment of the UN’s SDGs.

Meeting the UN SDGs targets while simultaneously growing the African economy requires an affordable and abundant energy source that can fulfil the expanding population needs of Africa, calling for all energy sources to be adopted in a different mix.

Renewable energy

Despite its immense potential, renewable energy alone is unsustainable for this purpose. Therefore, abundant natural gas reserves and their low-carbon credentials play a crucial role in meeting the competing trends of population growth and energy poverty needs in Africa. To achieve this, the projected demand growth of 82% by 2050 must be met by a set of energy sources with natural gas in the lead to fulfil the urgent urbanisation and industrialisation in Africa.

Africa can utilise its abundant gas reserves to meet its growing energy needs and fund its just and inclusive energy transition, which requires a combination of natural gas and renewables with CCUS technology in hard-to-abate sectors. Achieving this implies a purposeful capacity-building policy that facilitates in-house technological transformation, rapid skills transfer, and provides an enabling environment for higher education and research centres.

Furthermore, Africa being home to many Member Countries of the GECF, the gas export potential via pipelines, integrated African market for gas, and regional monetisation could benefit policy drive, maximising both the LNG and pipeline exports while providing much-needed within-continent growth. It is undeniable that Africa needs more affordable energy to achieve economic prosperity.-- TradeArabia News Service