Non-oil growth in GCC will offset oil output cut impact

MANAMA, March 13, 2019

The faster non-hydrocarbon growth will compensate for softer oil sector output in most parts of the GCC this year and this acceleration will help to cement popular support for ongoing gradual reforms and to curb increases in unemployment, said a report.

The main driver behind the acceleration in non-oil sector growth will be fiscal stimulus due to higher budgeted spending, except in Bahrain, where disbursements from the GCC Development Fund programme will offset cuts in investment spending, said the Moody's Investor Service report.

GCC countries will face weaker oil output this year compared to last year due to the production cuts agreed by Opec+ nations in December 2018, the report said.

Along with lower oil prices, this will put pressure on fiscal deficits and weaken external positions, especially in Oman (Ba1 negative), Bahrain (B2 stable), Saudi Arabia (A1 stable) and Kuwait (Aa2 stable), leading to faster debt accumulation than previously expected, it said.

The impact of weaker crude production on overall growth in 2019 will be commensurate with the expected decline in oil production and the share of the hydrocarbon sector in the total economy, which ranges from nearly 54% in Kuwait to less than 18% in Bahrain. Only Saudi Arabia and Oman will we see a deceleration in the overall growth rate compared to 2018, it added.

In Bahrain, progress on the project to modernise the national oil company (Bapco) and the ongoing expansion of Aluminum Bahrain (Alba) will support growth, the report continued. In Saudi Arabia, the completion of a major gas project and the large Jizan refinery coming online during the second half of 2019, as well as some initial progress on state-funded mega projects under Vision 2030, will bolster non-oil growth.

In the UAE, non-oil growth will primarily benefit from the disbursements from the $13.6 billion (3% of GDP) stimulus package that Abu Dhabi announced in June 2018 and will roll out during 2019-21.

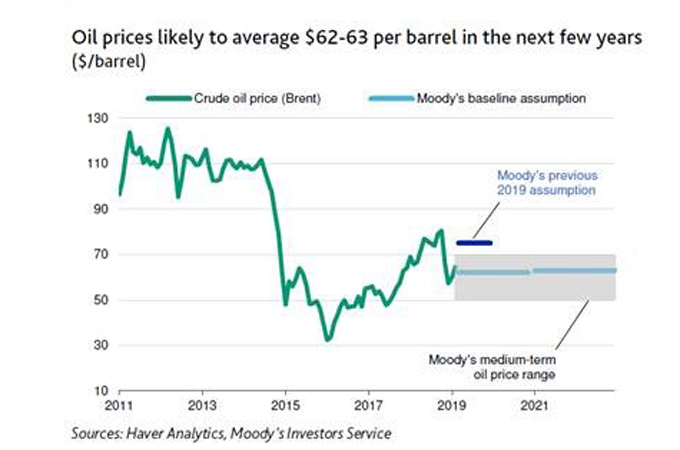

The report said oil prices are likely to remain moderate over medium term. It expected oil prices to

average $62 per barrel in 2019 and 2020, around the midpoint of its $50-70 medium-term

projection range and down from the $71 per barrel average in 2018.

Lower oil prices are expected to weaken GCC sovereigns’ fiscal positions, the report said. In 2019, the fiscal deficits are expected to widen by 6.9% of GDP in Kuwait, 3.7% in Oman, and 1.0% in Saudi Arabia, compared to our current estimates for 2018.

Higher budgetary spending will support a modest acceleration in non-hydrocarbon

growth in most countries. Despite weaker overall economic expansion, the expected

acceleration in non-oil growth will help to cement popular support for ongoing gradual

reforms and to curb increases in unemployment, it said.

The report said reduced oil output in combination with lower prices will weaken external

positions. "External pressures will be most pronounced in Oman, where we expect the

current account deficit to widen to 9.4% of GDP in 2019 from 5.3% in 2018. The ability

of the sovereign to retain access to external financing will be critical in preventing a

material erosion of central bank foreign exchange reserves. In Bahrain, external pressures

will be mitigated by the access to the GCC financial package, which we expect to cover

the government’s external debt service needs," it said.

The report said: "We believe a slowdown in global economic activity, further increases in crude stockpiles or unabated rapid production growth in the United States could see oil prices fall lower still. Conversely, continued production cuts by the Organization of Petroleum Exporting Countries (Opec) with Russia and Canada, as well as stricter enforcement of sanctions against Iran and Venezuela would help to prop up oil prices.

Given GCC countries' heavy dependence on exports of oil and gas, which drive current account balances and are also the main source of government revenue, lower prices will have a significant impact on the sovereigns' external and fiscal positions. Kuwait, Qatar and Oman would be most sensitive to a $10 per barrel change in oil price relative to the size of each country's GDP, it said.

"In the absence of additional reforms by governments in the region, we expect that moderate oil prices, well below the 2018 average of $71 per barrel, will put pressure on GCC countries' fiscal and external accounts over the coming few years," the report said.

For 2019, Moody's assumes that the UAE, Kuwait and Oman will maintain the 3% Opec+ cut, while Saudi Arabia will produce on average about 10.1 mbpd (a 5% cut from the October 2018 production level). However, since October production was significantly above the

annual average for most of the countries, the 3% cut implies a much smaller decline in annual production averages.

For the UAE, the 3% cut actually implies a 3% increase relative to the 2018 average, whereas in Saudi Arabia even a 5% cut from the October level will only reduce the average annual production rate by 2%. For Oman, we expect average annual production to decline by 1.3% in 2019. -TradeArabia News Service